Every year, the Secretary of State Audits Division conducts two major financial audits: the Annual Comprehensive Financial Report and Statewide Single Audit. Auditors also draft and release a report summarizing both of these audits. The summary report for fiscal year 2023, called Keeping Oregon Accountable, was released today.

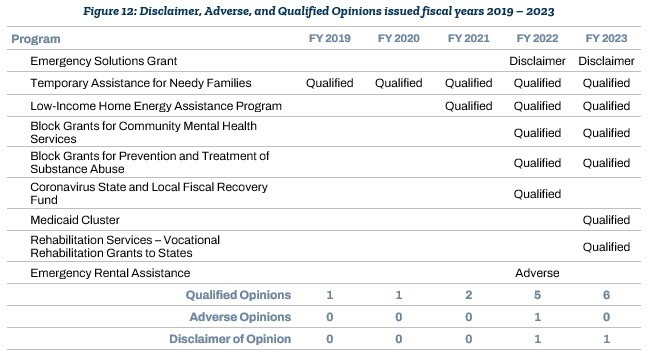

Last year’s summary report was somewhat of an anomaly, including the first adverse opinion and disclaimer of opinion issued by the Audits Division in more than 20 years. Auditors followed up on the findings that led to the unmodified opinions and found the agency had successfully taken corrective action to address the adverse opinion.

“This year’s Single Audit came with both good and bad news,” said Audits Director Kip Memmott. “I was very pleased to see the substantial corrective action to address last year’s adverse opinion. But there are still serious control weaknesses at other important programs that must be addressed, many of which have been ongoing for 10 or more years.”

The federal government requires audits of the state’s financial statements and compliance with federal program requirements for Oregon to continue receiving federal assistance. In the past, this funding has usually ranged from $11 to $12 billion each year, but federal funding has ballooned since the pandemic, exceeding $20 billion each year since fiscal year 2021. In fiscal year 2023, Oregon received $20.4 billion in federal aid.

Auditors found serious control weaknesses that, in some cases, have persisted for years. For fiscal year 2023, auditors issued six qualified opinions and a single disclaimer of opinion. No program was given an adverse opinion.

When an audit shows controls are sufficient and the program is generally in compliance with federal requirements, auditors issue an unmodified or “clean” opinion. Modified opinions — including qualified and disclaimer of — speak to the level of concern auditors have about the quality of internal controls.

A disclaimer of opinion was issued for the Emergency Solutions Grant Program at Oregon Housing and Community Services (OHCS). A disclaimer of opinion means there was not sufficient, appropriate evidence for auditors to even issue an opinion on program compliance. This program also received a disclaimer of opinion in fiscal year 2022.

Qualified opinions are less severe but indicate that internal controls are still inadequate to prevent or detect significant noncompliance. Auditors issued qualified opinions for six programs at three agencies: OHCS, the Oregon Department of Human Services, and the Oregon Health Authority. Two of these programs — Temporary Assistance for Needy Families, and the Low-Income Home Energy Assistance program — have been issued qualified opinions for several years now.

The federal granting agencies are responsible for following up on audit findings, as they have the authority to enforce grant requirements. Failure to address critical control weaknesses could include punitive consequences, like sanctions or a change in future funding, or it could be an opportunity for the granting agency to clarify its requirements.

Read the full report on the Secretary of State website.